Probability Distributions#

References#

https://stanford.edu/~shervine/teaching/cs-229/refresher-probabilities-statistics

https://www.amazon.in/Probability-Statistics-Machine-Learning-Fundamentals-ebook/dp/B00F5UGP0O

[54]:

import warnings

from graphpkg.static import plot_distribution

from IPython import display

import matplotlib.pyplot as plt

from matplotlib import animation

import numpy as np

import pandas as pd

from scipy import stats

import seaborn as sns

# plt.style.use('fivethirtyeight')

warnings.filterwarnings('ignore')

%matplotlib inline

Terminology#

\(P(Y=y) \text{ or } P(y)\)

Probabilities measure the likelihood of an outcome

A distribution is represented by these two parameters

Population

Sample

Represents

Mean \(\mu\)

Mean \(\bar{x}\)

Average Value

Variance \(\sigma^2\)

Variance \(s^2\)

Spread

Generally Variance doesn’t give an intuition of the spread. Hence to understand the deviation of the sample from the mean value, we use Standard Deviation \(\sigma\) / \(s\)

Exptected Value#

\begin{align*} \text{Expected Value }\mu &= E[(Y - \mu)^2] \\ &= E[Y]^2 - \mu^2 \\ \text{Spread }\sigma^2 &= E[(Y - \mu)^2] \\ &= E[Y]^2 - \mu^2 \end{align*}

Expected Value vs Mean#

Type of Distributions#

Discrete Distribution#

Finite number of outcomes

for eg - Rolling a dice, picking a card from a deck

Probabilty Mass Function

Discreete Random Variable

Continuous Distribution#

Infinite number of outcomes

Probability Density Function

Continuous Random Variable

Relation#

The CDF(Cumulative Density Function) gives the probability that a random variable X is less than or equal to any given number x.

It is important to understand that the notion of a CDF is universal to all random variables; it is not limited to only the discrete ones.

Scipy notations#

scipy function |

description |

|---|---|

Probability density function |

|

pmf |

Probability mass function |

cdf |

Cumulative distribution function |

ppf |

percent point function |

sf |

Survival function (1 – cdf) |

rvs |

Creating random samples from a distribution.(random variable samples) |

Understanding pmf and cdf#

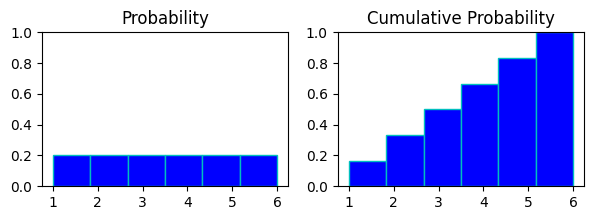

[2]:

data = np.linspace(start=1, stop=6, num=6, dtype="int")

fig, ax = plt.subplots(1, 2, figsize=(7, 2))

ax[0].hist(data, bins=6, density=True, edgecolor="c", color="b")

ax[0].set_xticks([1, 2, 3, 4, 5, 6])

ax[0].set_title("Probability")

ax[0].set_ylim([0, 1])

ax[1].hist(data, bins=6, density=True, cumulative=True, edgecolor="c", color="b")

ax[1].set_xticks([1, 2, 3, 4, 5, 6])

ax[1].set_title("Cumulative Probability")

ax[1].set_ylim([0, 1])

plt.show()

in above chart

probability chart of rolling a dice and cumulative probability chart of it.

in probabaility chart every digit has same probability of appearing on the roll of dice, hence all of them are at same height.

in cumulative prob chart evert digit(x) represents probabilities of digits<=x to appear on the roll.

like at bin 4 in cumul. prb.(rolling anything 4 or less) : p(x<=4) = p(x=1) + p(x=2) + p(x=3) + p(x=4)

Understanding pdf and cdf#

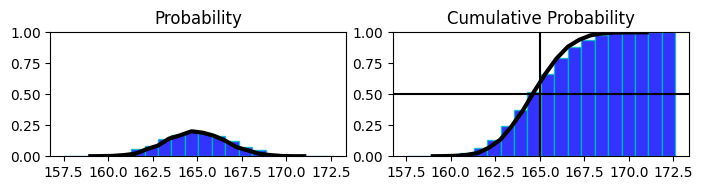

[3]:

np.random.seed(0)

bins = 20

mu = 165

sigma = 2

data = np.random.normal(loc=mu, scale=sigma, size=5000)

x = np.linspace(mu - sigma * 3, mu + sigma * 3, bins)

fig, ax = plt.subplots(1, 2, figsize=(7, 2))

n, _, _ = ax[0].hist(data, density=True, edgecolor="c", color="b", bins=bins, alpha=0.8)

ax[0].plot(x, n, "k", lw=3)

ax[0].set_title("Probability")

ax[0].set_ylim([0, 1])

n, _, _ = ax[1].hist(

data, density=True, cumulative=True, edgecolor="c", color="b", bins=bins, alpha=0.8

)

ax[1].plot(x, n, "k", lw=3)

ax[1].axhline(0.5, c="k")

ax[1].axvline(mu, c="k")

ax[1].set_title("Cumulative Probability")

ax[1].set_ylim([0, 1])

plt.tight_layout()

plt.show()

in above chart

proability distribution of heights of population with mean 165 and cumul. prob. of it on the right side.

on the right side at 0.5 mark on y shows that 50% of population has hight less than or equal to 165 (or we have accumulated 50% of distribution till 165)

probability density function f(x) \(\leftarrow \frac{\partial F{x}}{\partial x} \leftarrow\) cumulative probability function F(x)

probability density function f(x) \(\rightarrow \int_{-\infty}^{x} f(x) dx = F(x) \rightarrow\) cumulative probability function F(x)

Discrete Distribution#

Bernoulli Distribution#

Only one trial/ event

Only two possible outcomes

Like flipping a coin once.

Bernoulli Distribution is represented as

\begin{align*} X \sim Bern(p) \end{align*}

Variable X follows a Bernoulli Distribution with probability of success is p.

Conventionally p > 1-p , hence bigger probability is denoted by 1 and smaller probability is denoted by 0.

Probability Function#

\begin{align*} P(y;p) &\begin{cases} p && \text{if } y = 1 \\ 1-p && \text{if } y = 0 \end{cases}\\ &\text{or}\\ P(y;p) &= p^y . (1-p)^{(1- y)} \text{ , where } y \isin \{0, 1\} \end{align*}

Expected Value#

\begin{align*} E(X) &= 1. p + 0. (1-p) \\ E(X) &= p \\ \\ \sigma^2 &= (x_0 - \mu)^2 .P(x_0) + (x_1 - \mu)^2 . P(x_1) \\ \sigma^2 &= p.(1 - p) \end{align*}

[6]:

def plot_bernoulli_distribution(p):

bern_dist = stats.bernoulli(p=p)

mean, var, skew, kurt = bern_dist.stats(moments="mvsk")

print(f"""

Mean : {mean:.3f}

Variace : {var:.3f}

Skew : {skew:.3f}

Kurtosis: {kurt:.3f}

""")

data = np.arange(0, 2, 1, dtype=np.int32)

pmf = bern_dist.pmf(data)

fig, ax = plt.subplots(1, 1, figsize=(4, 2))

ax.bar(data, pmf, alpha=0.4, lw=3)

ax.plot(data, pmf, "k.")

for x, y in zip(data, pmf):

ax.text(x, y, s=round(y, 2))

ax.set_xticks(data)

ax.set_xlabel("Possible Outcomes")

ax.set_ylabel("Probability")

plt.legend()

plt.show()

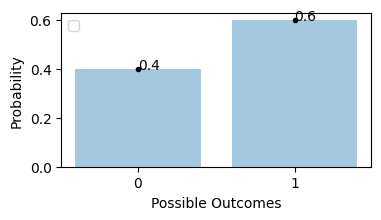

Examples#

Flipping an unfair coin, probability of getting tails is 0.6

[7]:

plot_bernoulli_distribution(0.6)

No artists with labels found to put in legend. Note that artists whose label start with an underscore are ignored when legend() is called with no argument.

Mean : 0.600

Variace : 0.240

Skew : -0.408

Kurtosis: -1.833

Binomial Distribution#

A number of times repeated bernoulli trials, as per definition limited to only 2 possible outcomes, where there is one outcome considered as success/favourable, and each trial is indepedent.

It is reprensented as \begin{align} X &\sim B(n, p) \\ \text{where } \\ n &= \text{number of trials}\\ p &= \text{probability of success in each trial} \end{align}

For example, dataset X follows a binomial distribution with 10 trials with each trial has a likelihood of getting success is 0.6

\begin{align} X &\sim B(10, 0.6) \end{align}

if there is only one trial then binomial distribution and bernoulli distribution is related \begin{align} Bern(p) = B(1, p) \end{align}

Like in a quiz where each question has only right and wrong answers -

Getting one question right is a bernoulli event.

Getting the entire quiz right is binomial event.

E[Bernoulli] = Expected outcome for a single trial

E[Binomial] = Number of times we expect to get a specific outcome

Probability Function#

The probability distribution function of the possible number of successful outcomes in a given number of trials, where the probability of success is same in each of them.

\begin{align} \text{If } n &= \text{number of trials}\\ y &= \text{number of success results}\\ P(\text{desired outcome}) &= p = \text{probability of success}\\ P(\text{alternative outcome}) &= 1-p = \text{probability of failure}\\ \end{align}

\begin{align*} B(y;n,p) &= \binom{n}{y}.{p^y}.{(1-p)}^{(n-y)} \\ \text{Where } \\ \binom{n}{y} &= \text{number of combinations favourable}\\ n &= \text{number of trials}\\ y &= \text{number of success results}\\ P(\text{desired outcome}) &= p = \text{probability of success}\\ P(\text{alternative outcome}) &= 1-p = \text{probability of failure}\\ \end{align*}

Flipping an unbiased coin 3 times , proability of getting exactly 2 tails

possible combinations will be

\begin{align*} \binom{n}{y} &= C_{y}^{n} = \text{y out of n combinations are favourable}\\ C_{2}^{3} &= 3 \text{ combinations shown below}\\ \\ &\begin{bmatrix} H & T & T \\ T & H & T \\ T & T & H \end{bmatrix} \end{align*}

then the calculation will be

\begin{align*} n &= \text{number of trials} = 3\\ y &= \text{number of success, getting tails} = 2\\ P(\text{desired outcome}) &= p = \text{probability of success} = 0.5\\ B(2; 3, 0.5) &= \binom{3}{2} (0.5)^2 (0.5)^1\\ &= 0.375 \end{align*}

37.5% chance is that we’ll get 2 tails while flipping a coin 3 times in a row.

Expected Value#

\begin{align*} E(X) &= X_0 P(X_0) + X_1 P(X_1) + ... + X_n P(X_n)\\ y &\sim B(n, p)\\ E(Y) &= \mu = n.p\\ \\ \sigma^2 &= E(Y^2) - [E(Y)]^2 = n.p.(1 - p)\\ \end{align*}

[8]:

def plot_binomial_distribution(n, p, show_text=True, figsize=(4, 2)):

binom_dist = stats.binom(n=n, p=p)

mean, var, skew, kurt = binom_dist.stats(moments="mvsk")

print(f"""

Mean : {mean:.3f}

Variace : {var:.3f}

Skew : {skew:.3f}

Kurtosis: {kurt:.3f}

""")

data = np.arange(0, n + 1, step=1, dtype=np.int64)

fig, ax = plt.subplots(1, 1, figsize=figsize)

pmf = binom_dist.pmf(data)

ax.plot(data, pmf, "k.", label="pmf")

if show_text:

for x, y in zip(data, pmf):

ax.text(x, y, s=round(y, 3))

ax.bar(data, pmf, color="orange", edgecolor="white", alpha=0.7)

if len(data) < 10:

ax.set_xticks(data)

ax.set_ylabel("Probability of Success")

ax.set_xlabel("Number of Success/favourable trials")

plt.legend()

plt.tight_layout()

Examples#

for n trials there will be n+1 bars in the distribution

[9]:

plot_binomial_distribution(n=5, p=0.5)

Mean : 2.500

Variace : 1.250

Skew : 0.000

Kurtosis: -0.400

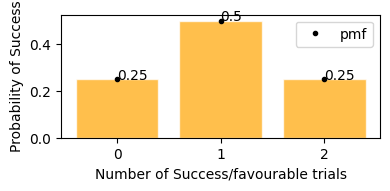

Flipping a coin 2 times, probability of getting head

[10]:

plot_binomial_distribution(n=2, p=0.5)

Mean : 1.000

Variace : 0.500

Skew : 0.000

Kurtosis: -1.000

Probability of getting 0 or 2 heads is 25%, and getting exactly 1 head probability is 50%.

[11]:

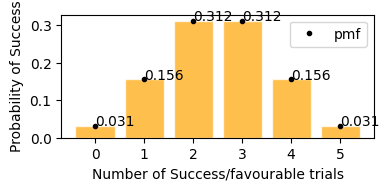

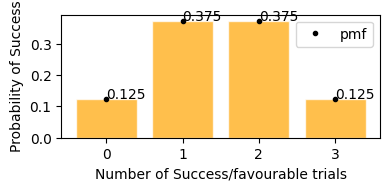

plot_binomial_distribution(n=3, p=0.5)

Mean : 1.500

Variace : 0.750

Skew : 0.000

Kurtosis: -0.667

This plot represents on x axis as success events and y is the probability of that happening.

In plot above, we can see the same result,

getting exactly 2 tails - 37.5%

getting exactly 1 tails - 37.5%

getting exactly no tails - 12.5%

getting exactly 3 tails - 12.5%

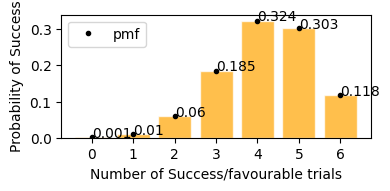

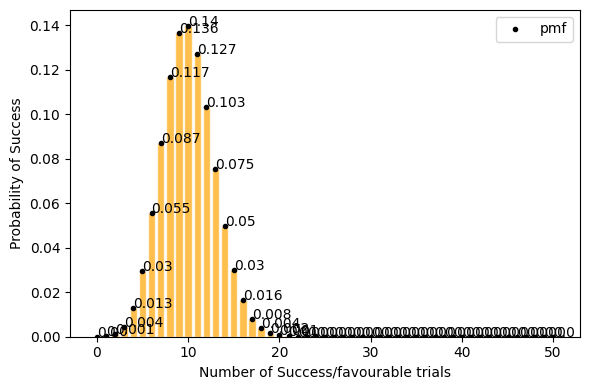

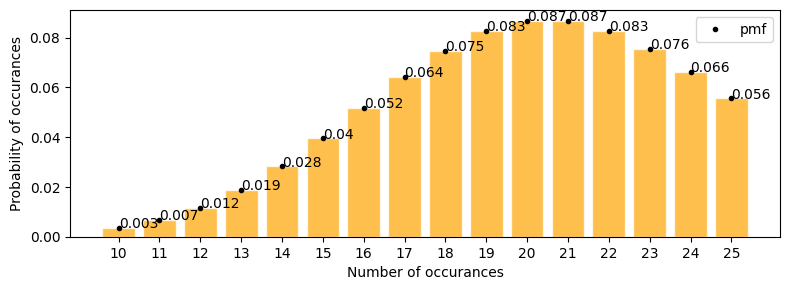

We are going to plan for next 6 days for the stock of Tata Motors The patterns show -

Chances of increament in value : P(increase) = 0.7

Chances of drop in value : P(decrease) = 0.3

First lets plot the binomial distribution for the use case

[12]:

plot_binomial_distribution(n=6, p=0.7)

Mean : 4.200

Variace : 1.260

Skew : -0.356

Kurtosis: -0.206

According to plot above

Probability of stock to increase exactly 3 days in next 6 days would be = 18.5%

Probability of stock to increase exactly 5 days in next 6 days would be = 30.3%

Probability of stock to increase exactly 4 days in next 6 days would be = 32.4%

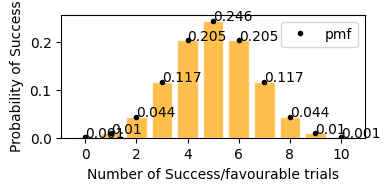

In case of coin flip 10 times, getting tails p(sucess rate) = 0.5 (50%), so in the graph it is visible that in 10 trials, getting exactly 5 successes(Heads) has the highest probability, similarly getting around 4 and 6 heads also have high probability, in same way getting only 2 (<5) or getting 8 (>5) successes has a very low probability.

[13]:

plot_binomial_distribution(n=10, p=0.5)

Mean : 5.000

Variace : 2.500

Skew : 0.000

Kurtosis: -0.200

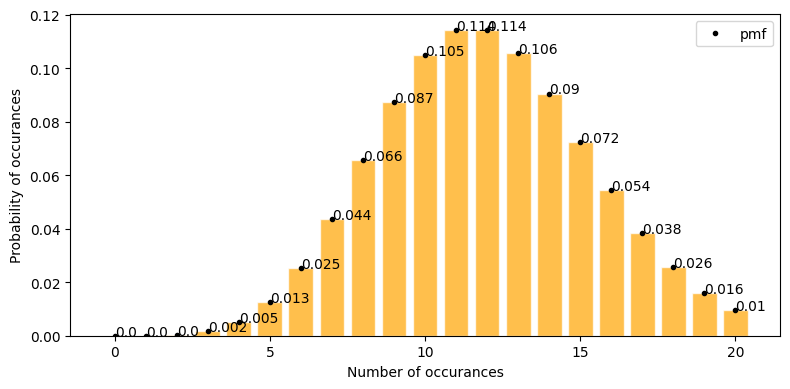

now lets take only 0.2(20%) success rate (getting tails) for 50 events. Here with success rate of 14% getting 10 tails in 50 trials has highest probability. and getting 25 tails (50% of the times) out of 50 trials is ~0 .

[14]:

plot_binomial_distribution(n=50, p=0.2, figsize=(6, 4))

Mean : 10.000

Variace : 8.000

Skew : 0.212

Kurtosis: 0.005

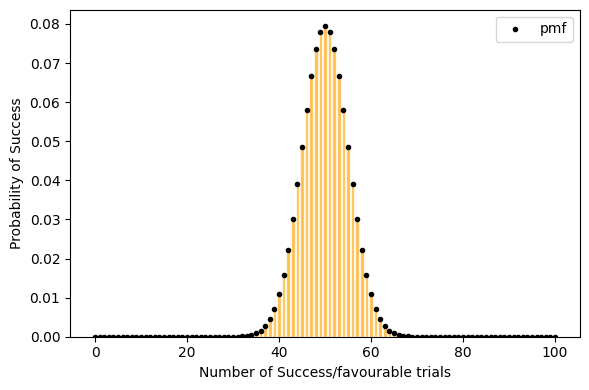

but for a large data set(a lot of trials, big n) Probability of success P is neither close to 0 or 1. the binomial distribution can be approximated by normal distribution. see below.

[15]:

plot_binomial_distribution(n=100, p=0.5, show_text=False, figsize=(6, 4))

Mean : 50.000

Variace : 25.000

Skew : 0.000

Kurtosis: -0.020

Poisson Distribution#

It is represented by

- :nbsphinx-math:`begin{align}

Y sim Po(lambda)

end{align}`

Variable Y follows a Poisson Distribution with \(\lambda\)

Poisson Distribution deals with a frequency with which an event occurs at a specific interval,

Instead of probability of event.How often it occurs for a specific time & distance.

Events occuring in a fixed time interval or region of oppotunity.

only needs one parameter, expected number of events per region/time interval

Average number of successes(\(\lambda\)) that occurs in a specified region is known

Unlike binomial distribution, Poisson continues to go on forever, hence distributioon is bounded by 0 and \(\infty\)

So we have assumptions also

The rate at which event occur is constant.

events are independent(one event doesn’t affect other events)

Probability Function#

\begin{align*} P(y; \lambda) &= \frac{\lambda^y e^{-\lambda}}{y!}\\ \\ \text{where } \\ \lambda &= \text{average frequency of occurance} \\ e &= \text{euler's number} \approx 2.718 \\ \end{align*}

[16]:

def plot_poisson_distribution(lambda_, a=0, b=10, show_text=True, figsize=(7, 2)):

poisson_dist = stats.poisson(lambda_)

mean, var, skew, kurt = poisson_dist.stats(moments="mvsk")

print(f"""

Mean : {mean:.3f}

Variace : {var:.3f}

Skew : {skew:.3f}

Kurtosis: {kurt:.3f}

""")

data = np.arange(a, b+1, step=1, dtype=np.int64)

fig, ax = plt.subplots(1, 1, figsize=figsize)

pmf = poisson_dist.pmf(data)

ax.plot(data, pmf, "k.", label="pmf")

if show_text:

for x, y in zip(data, pmf):

ax.text(x, y, s=round(y, 3))

ax.bar(data, pmf, color="orange", edgecolor="white", alpha=0.7)

if len(data) < 20:

ax.set_xticks(data)

ax.set_ylabel("Probability of occurances")

ax.set_xlabel("Number of occurances")

plt.legend()

plt.tight_layout()

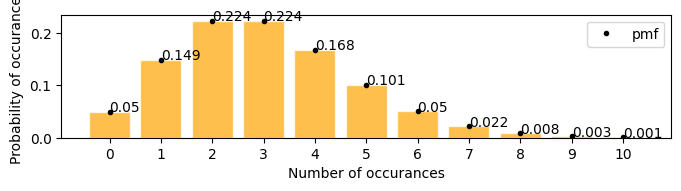

A firecracker launches 3 times in every 25 seconds, in the next 25 seconds what is the probability that it will launch exactly 6 times

[17]:

plot_poisson_distribution(3)

Mean : 3.000

Variace : 3.000

Skew : 0.577

Kurtosis: 0.333

there is 0.05(5%) chances that the firecracker might launch exactly 6 times in the next 25 seconds

Expected Value#

\begin{align*} E[y] &= y_0 \times P(y_0) + y_1 \times P(y_1) + ... \\ &= y_0 \times \frac{\lambda^{y_0} e^{-\lambda}}{y_0!} + ... \\ E[y] = \mu &= \lambda \\ \\ \sigma^2 &= \lambda \end{align*}

[18]:

plot_poisson_distribution(4)

Mean : 4.000

Variace : 4.000

Skew : 0.500

Kurtosis: 0.250

Examples#

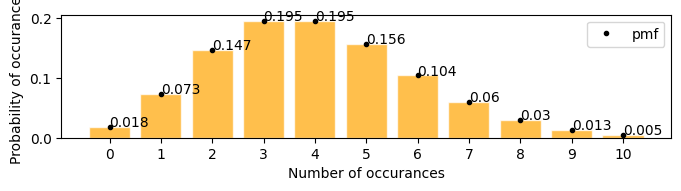

Number of defective products in a factory are 21 per day. what is the probability that the number will be 12 tomorrow

[19]:

plot_poisson_distribution(lambda_=21, a=10, b=25, figsize=(8, 3))

Mean : 21.000

Variace : 21.000

Skew : 0.218

Kurtosis: 0.048

according to the plot above \(\approx\) 0.012

lets solve with pdf \begin{align*} P(y; 21) &= \frac{21^y e^{-21}}{y!} \\ p(12; 21) &= \frac{21^{12} e^{-21}}{12!} \end{align*}

[20]:

round((21**12) * (np.exp(-21)) / np.math.factorial(12), 3)

[20]:

0.012

there is a website with a feature to but stuff online. Now the study is between number of clicks vs those clicks leading to an actual sale. now lambda or mu or mean click thorugh sales per day is 12.

exactly 10 click through sales in a day.

at least 10 click through sales in a day.

in below graph we can see

[21]:

plot_poisson_distribution(12, a=0, b=20, figsize=(8, 4))

Mean : 12.000

Variace : 12.000

Skew : 0.289

Kurtosis: 0.083

exactly 10 click through sales in a day = 0.105

at least 10 click through sales in a day

[22]:

stats.poisson.pmf(range(10, 30), mu=12).sum()

[22]:

0.7575989681906888

but here the assumption is rate at which these events(clicks) are occuring is constant. In real world I don’t think it can be regulated/ or profitable to regulate clicks per time interval.

Hypergeometric Distribution#

Equivalent to the

binomial distributionbutwithout replacement.Only two outomes are possible.

Card playing analogy comes in picture as if

one card is drawn from the deck then proabilities are changed for all the other cards to be drawn next.

If the card is again put in deck then all cards to be drawn has same prob again and it converts into

binomial.

Probability Function#

\begin{align*} P(y; N,Y,n) &= \frac{\binom{Y}{y} \binom{N-Y}{n-y}}{\binom{N}{n}}\\ \\ \text{where }\\ N &= \text{ total population size}\\ Y &= \text{ total item of interest in population}\\ n &= \text{ sample size}\\ y &= \text{ items of intereset in sample}\\ \end{align*}

Expected Value#

\begin{align*} E[Y] = \mu &= \frac{n.Y}{N}\\ \\ \sigma^2 &= n.\frac{Y}{N}.\frac{N-Y}{N}.\frac{N-n}{N-1}\\&= \frac{n.Y.(N-Y).(N-n)}{N^2.(N-1)} \end{align*}

[4]:

def plot_hypergeom_distribution(N, Y, n, show_text=True, figsize=(4, 2)):

hypergeom_dist = stats.hypergeom(M=N, n=Y, N=n)

mean, var, skew, kurt = hypergeom_dist.stats(moments="mvsk")

print(f"""

Mean : {mean:.3f}

Variace : {var:.3f}

Skew : {skew:.3f}

Kurtosis: {kurt:.3f}

""")

data = np.arange(0, n+1, step=1, dtype=np.int64)

fig, ax = plt.subplots(1, 1, figsize=figsize)

pmf = hypergeom_dist.pmf(data)

ax.plot(data, pmf, "k.", label="pmf")

if show_text:

for x, y in zip(data, pmf):

ax.text(x, y, s=round(y, 3))

ax.bar(data, pmf, color="orange", edgecolor="white", alpha=0.7)

if len(data) < 20:

ax.set_xticks(data)

ax.set_ylabel("Probability of occurances")

ax.set_xlabel("Number of occurances")

plt.legend()

plt.tight_layout()

Example#

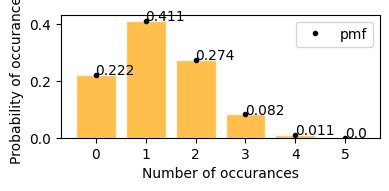

Probability fo getting cards of spades in a 5 card poker game.

Total cards total population size(N) = 52

total item of interest in population(Y) = 13 (number of spades)

sample size(n)= 5

items of intereset in sample y = ranging from 0 to 5

[8]:

plot_hypergeom_distribution(N=52, Y=13, n=5)

Mean : 1.250

Variace : 0.864

Skew : 0.452

Kurtosis: -0.179

What is the probability of drawing 2 spades in 5 card poker game.

now y = 2; p(2; 52, 13, 5) = ?

from graph when y = 2 P(2; 52, 13, 5) = 0.274

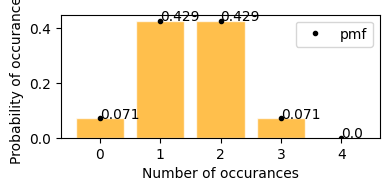

A wallet contains 3 100 dollar bills and 5 1 dollar bills. You randomly choose 4 bills. What is the probability that you will choose exactly 2 $100 bills?

total population of bills N = 8 bills (3100 + 51)

total 100 dollar bills X = 3

Sample size n = 4

probability of getting exactly 2 100 dollar bills from sample p(2; 8, 3, 4)

[9]:

plot_hypergeom_distribution(N=8, Y=3, n=4)

Mean : 1.500

Variace : 0.536

Skew : 0.000

Kurtosis: -0.293

according to the graph above -

probability of getting exactly 2 100 dollar bills from sample p(2; 8, 3, 4) = 0.429

Continuous Distribution#

Uniform Distribution#

A continuous random variable X is said to have a Uniform distribution over the interval [a,b], shown as

\begin{align} X &\sim U(a,b) \end{align}

Variable X follows a Uniform distribution ranging from a to b.

All outcomes have equal probability

like rolling a standard dice and getting any value from 1 to 6

Probability Function#

\begin{align} \text{ PDF is given by}\\ P(y; a, b) &= \begin{cases} \frac{1}{b-a} && a \le y \le b\\ 0 && \text{ else}\\ \end{cases}\\ \end{align}

Expected Value#

\begin{align} \text{Expected Value} = \mu &= \frac{a+b}{2}\\ \text{Variance} = \sigma^2 &= \frac{1}{12}{(b-a)^2} \end{align}

[ ]:

def plot_uniform_distribution(a, b, figsize=(4, 3), show_text=True):

uniform_dist = stats.uniform(loc=a, scale=b-a)

mean, var, skew, kurt = uniform_dist.stats(moments="mvsk")

print(f"""

Mean : {mean:.3f}

Variace : {var:.3f}

Skew : {skew:.3f}

Kurtosis: {kurt:.3f}

""")

data = np.arange(start=a, stop=b, step=1)

fig, ax = plt.subplots(1, 1, figsize=figsize)

pmf = uniform_dist.pdf(data)

ax.plot(data, pmf, "k.")

if show_text:

for x, y in zip(data, pmf):

ax.text(x, y, s=round(y, 3))

ax.bar(data, pmf, color="orange", edgecolor="white", alpha=0.7)

if len(data) < 10:

ax.set_xticks(data)

ax.set_ylabel("Probability")

ax.set_xlabel("Possible outcomes")

plt.tight_layout()

plt.show()

Example#

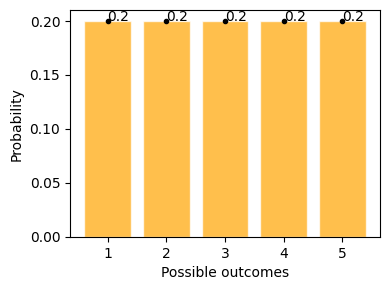

Rolling a standard dice

[ ]:

plot_uniform_distribution(1, 6)

Mean : 3.500

Variace : 2.083

Skew : 0.000

Kurtosis: -1.200

This example shows possible outcomes of rolling a standard dice, where getting 1 to 6 has equal possibility of 20%

Normal(Gaussian) Distribution#

the normal distribution is by far the most important probability distribution. One of the main reasons for that is the Central Limit Theorem (CLT)

area under the curve(AUC) = 1

say x \(\in R\), x is distributed Gaussian with mean \(\mu\) , variance \(\sigma^2\), standard deviation \(\sigma\)

\begin{align*} x &\sim N(\mu, \sigma^2) \end{align*}

Probability Function#

\begin{align*} P(x) &= \frac{1}{\sqrt{2.\pi.\sigma^2}} \exp\left( -\frac{1}{2}\left(\frac{x-\mu}{\sigma}\right)^{\!2}\,\right)\\ \end{align*}

Expected Value#

\begin{align*} \mu &= \frac{1}{m}\sum_{i=1}^{m}x^{(i)}\\ \sigma &= \frac{1}{m}\sum_{i=1}^{m}(x^{(i)} - \mu)^2 \end{align*}

[65]:

def plot_normal_distribution(mu, sigma, bins=15, show_text=True, figsize=(4, 2)):

norm_dist = stats.norm(loc=mu, scale=sigma)

mean, var, skew, kurt = norm_dist.stats(moments="mvsk")

std_dev = np.sqrt(var)

print(f"""

Mean : {mean:.3f}

Variace : {var:.3f}

Skew : {skew:.3f}

Kurtosis: {kurt:.3f}

""")

fig, ax = plt.subplots(1, 1, figsize=figsize)

data = norm_dist.rvs(1000, random_state=1)

counts, bins = np.histogram(data, bins=bins, density=False)

probs = counts/ counts.sum()

ax.hist(bins[:-1], bins, weights=probs, edgecolor='white', color='green')

if show_text:

for x, y in zip(bins, probs):

ax.text(x, y, s=round(y, 2))

fig.tight_layout()

return fig, ax

[66]:

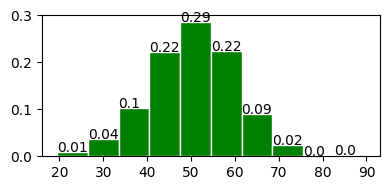

fig, ax = plot_normal_distribution(50, 10, 10)

Mean : 50.000

Variace : 100.000

Skew : 0.000

Kurtosis: 0.000

[82]:

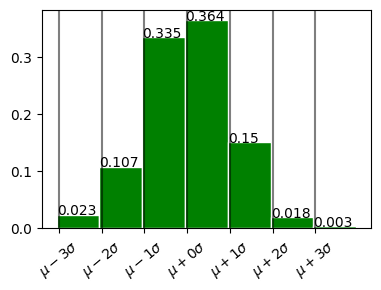

norm_dist = stats.norm(loc=0, scale=1)

mean, var, skew, kurt = norm_dist.stats(moments="mvsk")

std_dev = np.sqrt(var)

fig, ax = plt.subplots(1, 1, figsize=(4,3))

data = norm_dist.rvs(1000, random_state=1)

counts, bins = np.histogram(data, bins=7, density=False)

probs = counts/ counts.sum()

ax.hist(bins[:-1], bins, weights=probs, edgecolor='white', color='green')

for x, y in zip(bins, probs):

ax.text(x, y, s=round(y, 5))

vals = []

labels = []

for a in range(-3, 4, 1):

l = mean + (a * np.sqrt(var))

vals.append(l)

labels.append(f"$\mu {'-' if a<0 else '+'}{abs(a)}\sigma$")

ax.axvline(x=l, c='k', alpha=0.5)

ax.set_xticks(vals, labels, rotation=40)

fig.tight_layout()

In plot above

68% within 1 standard deviation \(\mu \pm \sigma\)

98% within 2 standard deviation. \(\mu \pm 2\sigma\)

99.7% within 3 standard deviation. \(\mu \pm 3\sigma\)

Standard Normal Distribution (z Distribution)#

normal distribution with mean = 0 and standard deviation = 1.

[74]:

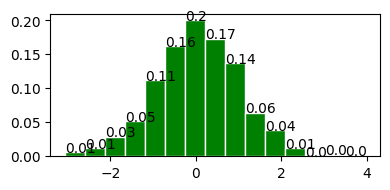

plot_normal_distribution(0, 1);

Mean : 0.000

Variace : 1.000

Skew : 0.000

Kurtosis: 0.000

Coverting to z-scores (Standardization/ Normalization)#

Converting data to z-scores(normalizing or standardizing) doesn’t convert the data to normal distribution,

it just puts the data in the same scale as standard normal distribution.

Normalization Process subtract mean and devide by the standard deviation.

\begin{align*} z = \frac{x - \bar{x}}{\sigma} \end{align*}

Calculate auc with z-score#

Why the hell would I calculate z-score? TBD

[11]:

mu = 75

sigma = 10

bell_curve_data = np.random.normal(loc=mu, scale=sigma, size=(10000,))

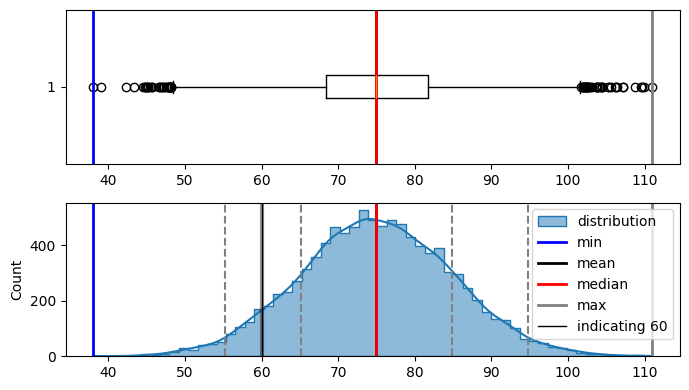

plot_distribution(bell_curve_data, indicate_data=[60], figsize=(7, 4))

Min : 38.057147077212285

Max : 110.98310102305439

Median : 74.90401793747884

Mode : ModeResult(mode=38.057147077212285, count=1)

Mean : 74.99552606711973

Std dev : 9.906804817099255

in the curve above i can see. i need to find z-score(area under the curve from left side only) for

-1.49.so lets look at the z score table

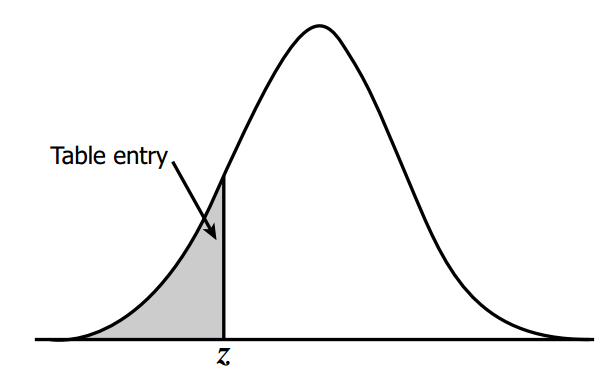

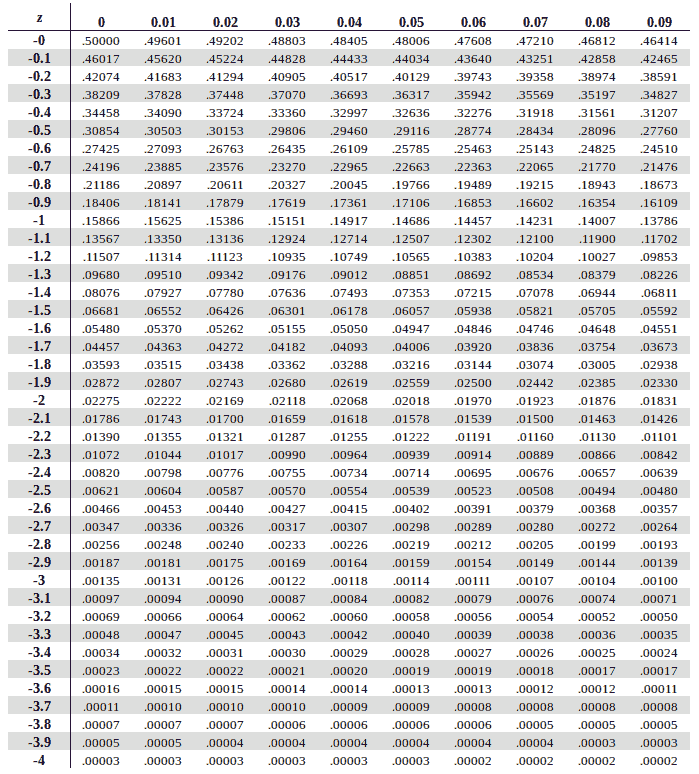

z-score table#

This table tells us area under the curve(probability in this case) based on z-score.

we need negative 1.49

so from top to bottom i’ll select -1.4

and from left to right i’ll select 0.09

i get 0.06811

[12]:

data = np.random.normal(loc=0, scale=1, size=1000)

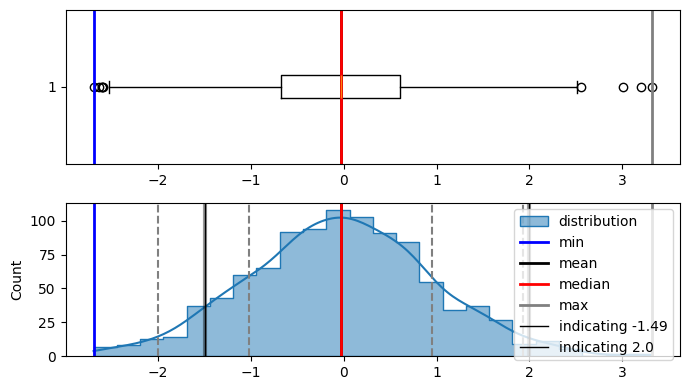

plot_distribution(data, indicate_data=[-1.49, 2.0], figsize=(7, 4))

Min : -2.693477658187908

Max : 3.321601166647714

Median : -0.026861025439324573

Mode : ModeResult(mode=-2.693477658187908, count=1)

Mean : -0.032810027367517494

Std dev : 0.9819687703292147

here in the diagram, area under the curve on the left side from -1.49 is 0.06811(6.8%) and 2.0 is 0.9772(97.72%). and this is correct also as -1.49 doesnt have a lot of data on the left side of it.

[13]:

stats.norm.ppf(0.06811) # percent point function

[13]:

-1.4900161102718568

[14]:

stats.norm.ppf(0.9772)

[14]:

1.9990772149717693

Central Limit Theorem#

The central limit theorem states that if you have a population with mean μ and standard deviation σ and take sufficiently large random samples from the population with replacement, then the distribution of the

sample meanswill be approximately normally distributed (we can use normal distribution statistic).simply for a population, increase number of samples then distribution moves towards normal distribution.

Central limit theorem allows normal-approximation formulas like t-distribution to be used in calculating sampling distributions for inference ie confidence intervals and hypothesis tests.

[15]:

pop_size = 5000

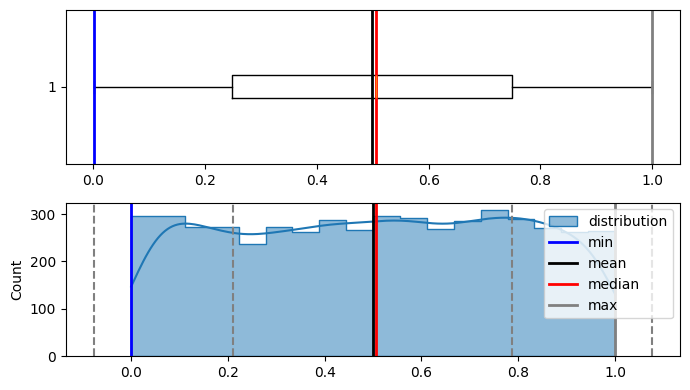

population = np.random.rand(pop_size)

plot_distribution(population, figsize=(7, 4))

Min : 0.00034494409119278924

Max : 0.9998556266062902

Median : 0.5058725592216615

Mode : ModeResult(mode=0.00034494409119278924, count=1)

Mean : 0.49948958836972196

Std dev : 0.288386913695571

As it is visible that population is not normally distributed.

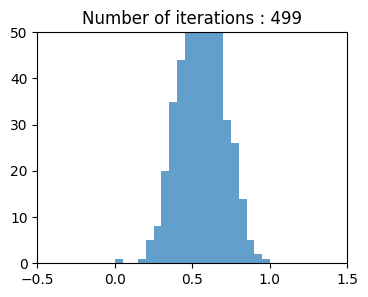

Now lets generate random sample from the iterations, calculate there means, and plot them iteration by iteration, although population wasn't normally distributed but according to CENTRAL LIMIT THEOREM means of resamples should be normally distributed.

[16]:

bins = 20

resampling_iterations = 500

sample_size = 500

sample = np.random.choice(population, size=sample_size)

sample_means = []

# sample_means.append(sample.mean())

fig = plt.figure(figsize=(4, 3))

ax1 = fig.add_subplot()

ax1.set_xlim(-0.5, 1.5)

ax1.set_ylim(0, 50)

_, _, container = ax1.hist(sample_means, bins=bins, density=True, alpha=0.7)

def draw_frame(n):

sample = np.random.choice(population, size=sample_size)

sample_means.append(sample.mean())

heights, _ = np.histogram(sample_means, bins=bins)

for height, rect in zip(heights, container.patches):

rect.set_height(height)

ax1.set_title(f"Number of iterations : {n}")

return container.patches

anim = animation.FuncAnimation(

fig, draw_frame, frames=resampling_iterations, interval=100, blit=True

)

display.HTML(anim.to_html5_video())

[16]:

Long Tailed Distribution#

Tail long narrow portion of a frequency dist. extreme values occur at low frequency.

most data is not normally distribution.

Chi-squared Distribution#

if a random variable \(Z\) has standard normal distribution then \(Z_1^2\) has the \(\chi^2\) distribution with one degree of freedom

if a random variable \(Z\) has standard normal distribution then \(Z_1^2 + Z_2^2\) has the \(\chi^2\) distribution with two degree of freedom

if \(Z_1,Z_2,...,Z_k\) are independent standard normal (distribution) random variables then \(Z_1^2 + Z_2^2 + ... + Z_k^2\) has the \(\chi^2\) distribution with k degrees of freedom

All these are actually explained below.

Probability Function#

\begin{align*} \text{Probability density function }f(x,k) = \begin{cases} \frac{1}{2^{(k/2)} \Gamma{(k/2)}} . x^{(k/2) -1}. e^{(-x/2)} & \text{for } x \ge 0\\ 0 & else \end{cases} \end{align*}

Where

k = degree of freedom

Gamma func \(\Gamma(x)=(x-1)!\)

Detailed intuition#

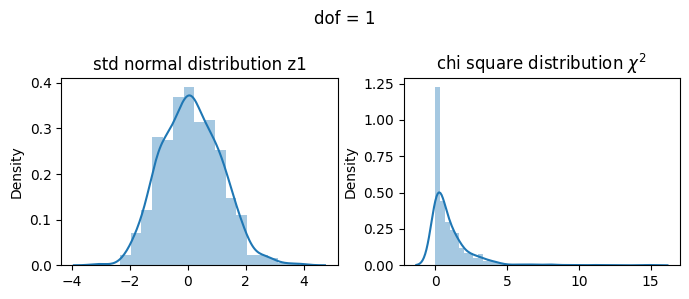

Can be thought of as the square of selection taken from a standard normal distribution Derivation \(\chi_k^2 = \sum_{i=1}^k Z_i^2\)

1 dof#

\(\chi^2 = Z_1^2\)

[17]:

z1 = np.random.normal(size=500)

X1 = z1**2

fig, ax = plt.subplots(1, 2, figsize=(7, 3))

sns.distplot(z1, ax=ax[0])

ax[0].set_title("std normal distribution z1")

sns.distplot(X1, ax=ax[1])

ax[1].set_title("chi square distribution $\chi^2$")

fig.suptitle("dof = 1")

plt.tight_layout()

plt.show()

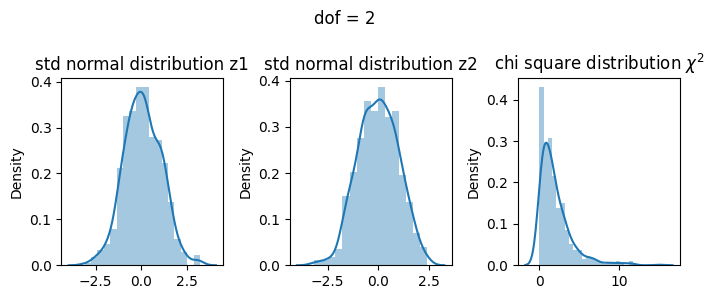

2 dof#

\(\chi^2= Z_1^2 + Z_2^2\)

[18]:

z1 = np.random.normal(size=500)

z2 = np.random.normal(size=500)

X2 = z1**2 + z2**2

fig, ax = plt.subplots(1, 3, figsize=(7, 3))

sns.distplot(z1, ax=ax[0])

ax[0].set_title("std normal distribution z1")

sns.distplot(z2, ax=ax[1])

ax[1].set_title("std normal distribution z2")

sns.distplot(X2, ax=ax[2])

ax[2].set_title("chi square distribution $\chi^2$")

fig.suptitle("dof = 2")

plt.tight_layout()

plt.show()

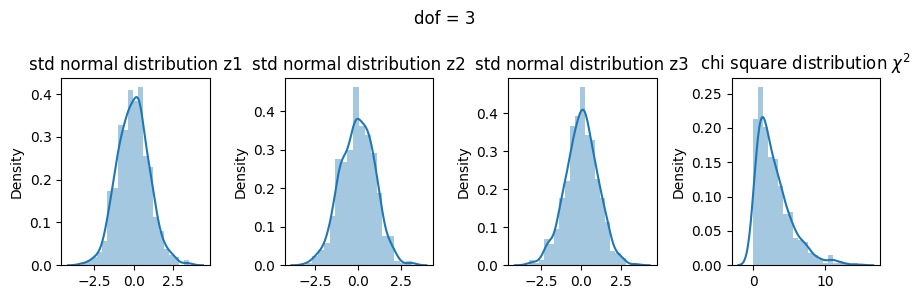

3 dof#

\(\chi^2 = Z_1^2 + Z_2^2 + Z_3^2\)

[19]:

z1 = np.random.normal(size=500)

z2 = np.random.normal(size=500)

z3 = np.random.normal(size=500)

X3 = z1**2 + z2**2 + z3**2

fig, ax = plt.subplots(1, 4, figsize=(9, 3))

sns.distplot(z1, ax=ax[0])

ax[0].set_title("std normal distribution z1")

sns.distplot(z2, ax=ax[1])

ax[1].set_title("std normal distribution z2")

sns.distplot(z3, ax=ax[2])

ax[2].set_title("std normal distribution z3")

sns.distplot(X3, ax=ax[3])

ax[3].set_title("chi square distribution $\chi^2$")

fig.suptitle("dof = 3")

plt.tight_layout()

plt.show()

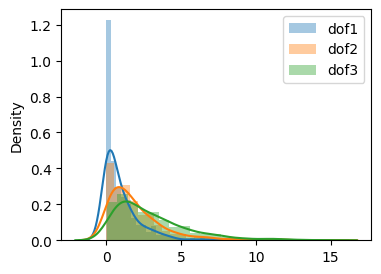

Comparing all three dof#

[20]:

fig, ax = plt.subplots(1, 1, figsize=(4, 3))

sns.distplot(X1, label="dof1", ax=ax)

sns.distplot(X2, label="dof2", ax=ax)

sns.distplot(X3, label="dof3", ax=ax)

plt.legend()

plt.show()

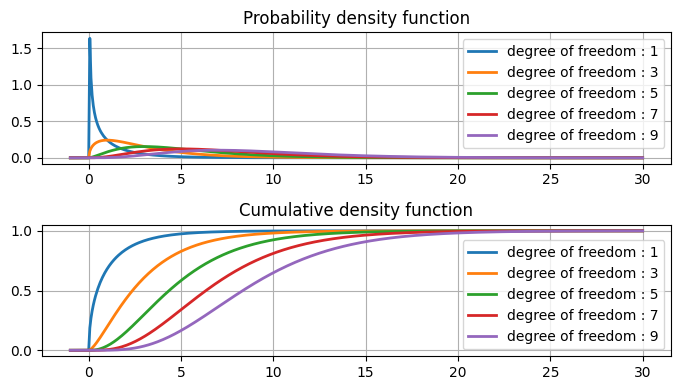

[21]:

fig, ax = plt.subplots(2, 1, figsize=(7, 4))

data = np.linspace(start=-1, stop=30, num=500)

for dof in range(1, 10, 2):

chi2_dist = stats.chi2(dof)

ax[0].plot(data, chi2_dist.pdf(data), label=f"degree of freedom : {dof}", lw=2)

ax[1].plot(data, chi2_dist.cdf(data), label=f"degree of freedom : {dof}", lw=2)

ax[0].legend(loc="best")

ax[0].grid()

ax[0].set_title("Probability density function")

ax[1].legend(loc="best")

ax[1].grid()

ax[1].set_title("Cumulative density function")

plt.tight_layout()

plt.show()

Chi-square table#

this table includes data point, area under the curve(first row) and degree of freedom(first column).

The areas given across the top are the areas to the right of the critical value. To look up an area on the left, subtract it from one, and then look it up (ie: 0.05 on the left is 0.95 on the right)

ref = https://people.richland.edu/james/lecture/m170/tbl-chi.html

Ref : https://people.richland.edu/james/lecture/m170/tbl-chi.html

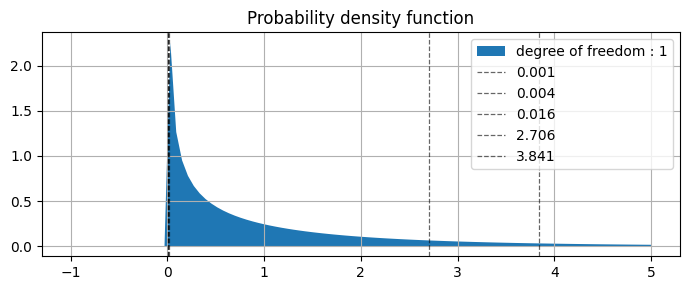

degree of freedom 1#

[22]:

fig, ax = plt.subplots(1, 1, figsize=(7, 3))

data = np.linspace(start=-1, stop=5, num=100)

dof = 1

chi2_dist = stats.chi2(dof)

ax.fill_between(data, chi2_dist.pdf(data), label=f"degree of freedom : {dof}", lw=2)

for i in [0.001, 0.004, 0.016, 2.706, 3.841]:

ax.axvline(i, c="k", linestyle="--", linewidth=0.9, alpha=0.6, label=i)

ax.legend(loc="best")

ax.grid()

ax.set_title("Probability density function")

plt.tight_layout()

plt.show()

from above plot we can see that

0.001 |

0.004 |

0.016 |

2.706 |

3.841 |

values are specifying |

0.975 |

0.95 |

0.90 |

0.10 |

0.05 |

AUC of the right side of the curve |

(picked values from table above)

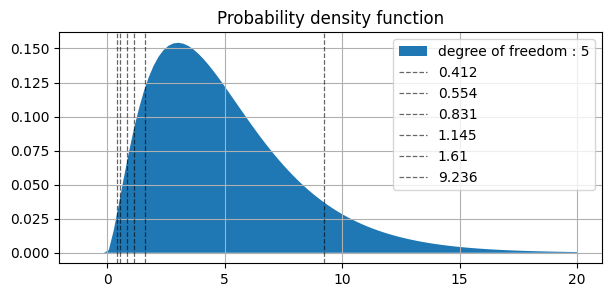

degree of freedom 5#

[23]:

fig, ax = plt.subplots(1, 1, figsize=(7, 3))

data = np.linspace(start=-1, stop=20, num=100)

dof = 5

chi2_dist = stats.chi2(dof)

ax.fill_between(data, chi2_dist.pdf(data), label=f"degree of freedom : {dof}", lw=2)

for i in [0.412, 0.554, 0.831, 1.145, 1.610, 9.236]:

ax.axvline(i, c="k", linestyle="--", linewidth=0.9, alpha=0.6, label=i)

ax.legend(loc="best")

ax.grid()

ax.set_title("Probability density function")

plt.show()

similarly in plot above ||||||| |-|-|-|-|-|-| | values | 0.412 | 0.554 | 0.831 | 1.145 | 1.610 | 9.236 | | AUC(right side) | 0.995 | 0.99 | 0.975 | 0.95 | 0.90 | 0.10 |

Student’s t distribition#

Small sample statistics.

Underlying distribution is normal.

Unknown population standard normal distribution.

Sample size too small to apply Central limit theorem.

Normally shaped distribution but thicker and long tails.

As degree of freedom increases t distribution tends towards the standard normal distribution.

Z has standard normal distribution, U has the \(\chi^2\) distribution with \(\nu\) degree of freedom. Z and U are independent.

Probability Function#

\begin{align*} t &= \frac{Z}{\sqrt{\frac{U}{\nu}}} \text{ has the t distribution with }\nu \text{ degree of freedom}\\ Z &= \frac{x - \mu}{\sigma}\\ \\ \text{ pdf }f(x, \nu) &= \frac{\Gamma (\frac{\nu + 1 }{2})}{\sqrt{\pi \nu} \Gamma (\frac{\nu}{2})}(1+ \frac{x^2}{\nu})^{-\frac{(\nu + 1)}{2}}\\ \\\nu &= n-1\\ \\ \mu &= 0 \text{ for } \nu < 1\\ \\ \sigma^2 &= \frac{\nu}{\nu - 2} for {\nu} > 2\\ \Gamma(x) &= (x-1)! \text{ Gamma Function} \end{align*}

Ref : https://en.wikipedia.org/wiki/Student%27s_t-distribution

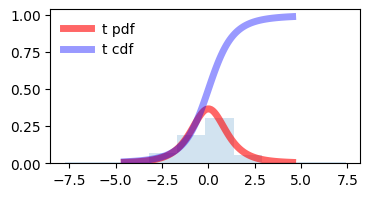

[24]:

fig, ax = plt.subplots(1, 1, figsize=(4, 2))

df = 3

size = 100

mean, var, skew, kurt = stats.t.stats(df, moments="mvsk")

x = np.linspace(stats.t.ppf(0.01, df), stats.t.ppf(0.99, df), size)

ax.plot(x, stats.t.pdf(x, df), "r-", lw=5, alpha=0.6, label="t pdf")

ax.plot(x, stats.t.cdf(x, df), "b-", lw=5, alpha=0.4, label="t cdf")

ax.hist(stats.t.rvs(df, size=size), density=True, histtype="stepfilled", alpha=0.2)

ax.legend(loc="best", frameon=False)

plt.show()

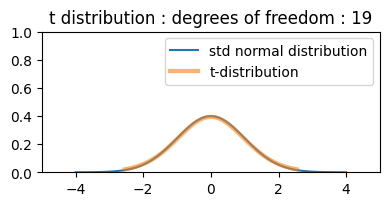

demonstraion on increasing degrees of freedom, t distribution approaches towards normal distribution. and it seems correct also as by increasing degrees of freedom (\(\nu\) = n - 1) we are increasing the sample size also.

[25]:

fig = plt.figure(figsize=(4, 2))

ax1 = fig.add_subplot()

ax1.set_xlim(-5, 5)

ax1.set_ylim(0, 1)

d = np.linspace(-4, 4, 100)

ax1.plot(d, stats.norm.pdf(d), label="std normal distribution")

(plot1,) = ax1.plot([], [], lw=3, alpha=0.6, label="t-distribution")

plt.legend(loc="best")

plt.tight_layout()

def draw_frame(n):

df = n

mean, var, skew, kurt = stats.t.stats(df, moments="mvsk")

x = np.linspace(stats.t.ppf(0.01, df), stats.t.ppf(0.99, df), 1000)

plot1.set_data(x, stats.t.pdf(x, df))

ax1.set_title(f"t distribution : degrees of freedom : {n}")

return (plot1,)

anim = animation.FuncAnimation(fig, draw_frame, frames=20, interval=1000, blit=True)

display.HTML(anim.to_html5_video())

[25]:

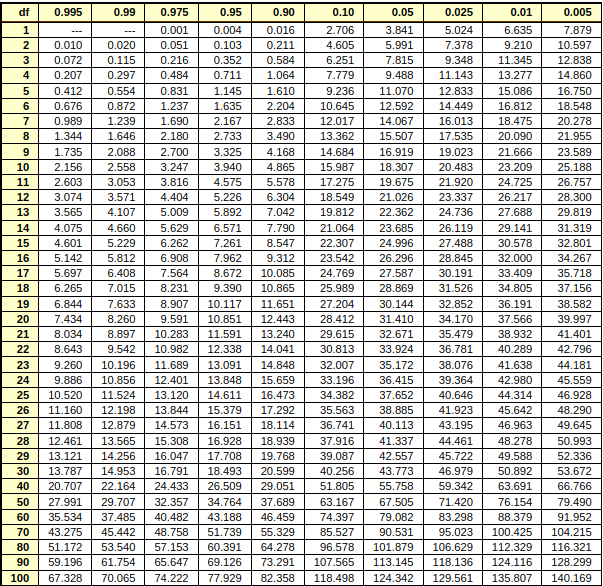

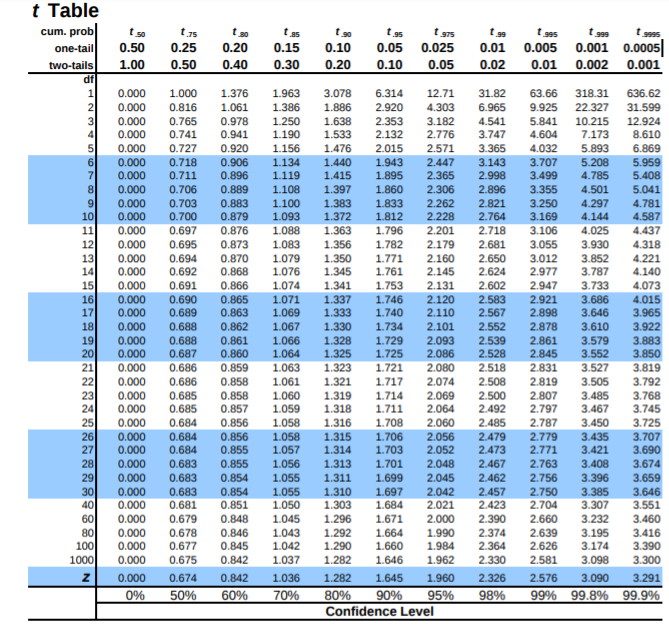

t table#

t table here shows degrees of freedom and cumulative distribution, probability distribution(one tail, two tails) and gives t-statistic.

Ref : https://www.sjsu.edu/faculty/gerstman/StatPrimer/t-table.pdf

Lets say we need to know what t-statistic with 4 df provides 2.5% in upper tail ? or we need to know the point above which lies 2.5% of the distribution.

the table tells us AUC. so actually we need to find the auc after the 2.5%(0.025) = 1 - 0.025 = 0.975

so either \(t_{0.975}\) or one tail 0.025. in table above for df 4 and given inputs then t-statistic = 2.776

or use scipy

[26]:

stats.t.ppf(0.975, 4)

[26]:

2.7764451051977987

[27]:

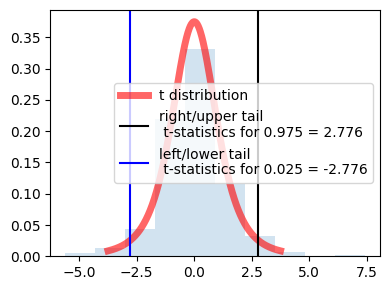

np.random.seed(10)

fig, ax = plt.subplots(1, 1, figsize=(4, 3))

df = 4

size = 500

p = 0.025 # 2.5%

mean, var, skew, kurt = stats.t.stats(df, moments="mvsk")

x = np.linspace(stats.t.ppf(0.01, df), stats.t.ppf(0.99, df), size)

ax.plot(x, stats.t.pdf(x, df), "r-", lw=5, alpha=0.6, label="t distribution")

ax.hist(stats.t.rvs(df, size=size), density=True, histtype="stepfilled", alpha=0.2)

right_t_stat = stats.t.ppf(1 - p, df)

left_t_stat = stats.t.ppf(p, df)

ax.axvline(

right_t_stat,

c="k",

label=f"right/upper tail \n t-statistics for {1-p} = {right_t_stat:.3f}",

)

ax.axvline(

left_t_stat,

c="b",

label=f"left/lower tail \n t-statistics for {p} = {left_t_stat:.3f}",

)

ax.legend(loc="best")

plt.tight_layout()

plt.show()

because of the symmetry values are same for left and right just the sign is opposite.

in the center actually it is showing 95% distribution (100 - 2.5 - 2.5)

F Distribution#

[28]:

dfn, dfd = 29, 18 # degree of fre

mean, var, skew, kurt = stats.f.stats(dfn, dfd, moments="mvsk")

x = np.linspace(stats.f.ppf(0.01, dfn, dfd), stats.f.ppf(0.99, dfn, dfd), 100)

fig, ax = plt.subplots(1, 1, figsize=(4, 2))

ax.plot(x, stats.f.pdf(x, dfn, dfd), "r-", lw=5, alpha=0.6, label="f pdf")

plt.tight_layout()

plt.show()

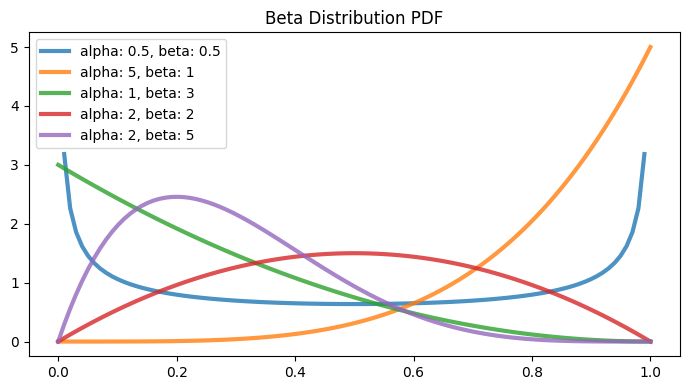

Beta Distribution#

Part of continuous probability distribution familily

within the interval [0, 1]

two positive shape parameters \(\alpha\) and \(\beta\), to shape the probability distribution

Probabilty Function#

\begin{align*} f(x; \alpha, \beta) &= \frac{x^{\alpha}(1-x)^{\beta}}{B(\alpha, \beta)}\\ \\ \text{ where }\\ B(\alpha, \beta) &= \frac{\Gamma(\alpha) \Gamma(\beta)}{\Gamma(\alpha + \beta)}\\ \Gamma(n) &= (n - 1)! \end{align*}

[29]:

parameters = [(0.5, 0.5), (5, 1), (1, 3), (2, 2), (2, 5)]

[30]:

fig, ax = plt.subplots(1, 1, figsize=(7, 4))

for a, b in parameters:

# print(a, b)

x = np.linspace(stats.beta.ppf(0, a, b), stats.beta.ppf(1, a, b), 100)

ax.plot(

x,

stats.beta.pdf(x, a, b),

alpha=0.8,

linewidth=3,

label=f"alpha: {a}, beta: {b}",

)

ax.set_title("Beta Distribution PDF")

ax.legend()

plt.tight_layout()

plt.show()

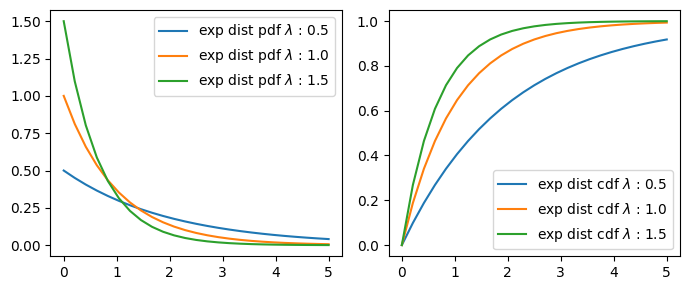

Exponential Distribution#

The time between events in a Poisson process (‘inverse’ of Poisson)

Poisson |

Exponential |

|---|---|

Number of cars passing a tollgate in one hour. |

Number of hours between car arrivals. |

Probability Function#

\(pdf(x;\lambda) = \begin{cases} \lambda e^{-\lambda x} & x \ge 0, \\ 0 & x < 0. \end{cases}\)

\(\lambda\) = rate(inverse scale) parameter/ exponentiation parameter.

or

\(pdf(x;\beta) = \begin{cases} \frac{1}{\beta} e^{-\frac{x}{\beta}} & x \ge 0, \\ 0 & x < 0. \end{cases}\)

\(\beta\) = scale parameter.

\(\lambda = \frac{1}{\beta}\)

Ref : https://en.wikipedia.org/wiki/Exponential_distribution

[31]:

class ExpDist:

def __init__(self, lambd):

self.lambd = lambd

def pdf(self, x):

return (self.lambd * (np.exp(-self.lambd * x))) * (x >= 0)

def cdf(self, x):

return (1 - np.exp(-self.lambd * x)) * (x >= 0)

[32]:

x = np.linspace(0, 5, 25)

x_tick_s = np.linspace(0, 5, 6)

fig, ax = plt.subplots(1, 2, figsize=(7, 3))

for l in np.arange(0.5, 2, 0.5):

y_pdf = ExpDist(l).pdf(x)

ax[0].plot(x, y_pdf, "-", label=f"exp dist pdf $\lambda$ : {l}")

ax[0].set_xticks(x_tick_s)

ax[0].legend()

for l in np.arange(0.5, 2, 0.5):

y_cdf = ExpDist(l).cdf(x)

ax[1].plot(x, y_cdf, "-", label=f"exp dist cdf $\lambda$ : {l}")

ax[1].set_xticks(x_tick_s)

ax[1].legend()

plt.tight_layout()

plt.show()

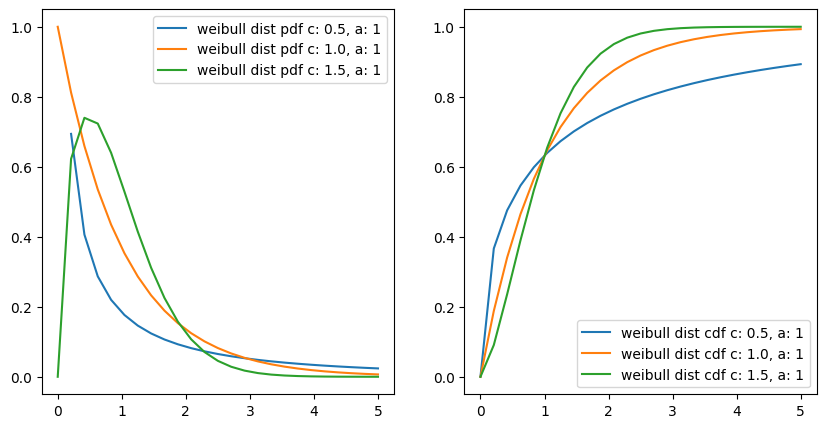

Weibull Distribution#

the event rate does not remain constant over time. If the period over which it changes is much longer than the typical interval between events, there is no problem; you just subdivide the analysis into the segments where rates are relatively constant, as mentioned before.

The Weibull distribution is an extension of the exponential distribution, in which the event rate is allowed to change, as specified by a shape parameter k.

Proability Function#

\(f(x;\beta,k) = \begin{cases} \frac{k}{\beta}\left(\frac{x}{\beta}\right)^{k-1}e^{-(x/ \beta)^{k}} & x\geq0 ,\\ 0 & x<0, \end{cases}\)

or

\(f(x;\lambda,k) = \begin{cases} k{\lambda} \left({\lambda}{x}\right)^{k-1}e^{-(\lambda x)^{k}} & x\geq0 ,\\ 0 & x<0, \end{cases}\)

a or \(\lambda\) is the exponentiation parameter.

\(\frac{1}{\beta}\) is the scale parameter.

c or \(k\) is the shape parameter of the non-exponentiated Weibull law.

[33]:

x = np.linspace(0, 5, 25)

x_tick_s = np.linspace(0, 5, 6)

fig, ax = plt.subplots(1, 2, figsize=(10, 5))

for i in np.arange(0.5, 2, 0.5):

y_pdf = stats.exponweib.pdf(x, a=1, c=i)

ax[0].plot(x, y_pdf, "-", label=f"weibull dist pdf c: {i}, a: 1")

ax[0].set_xticks(x_tick_s)

ax[0].legend()

for i in np.arange(0.5, 2, 0.5):

y_cdf = stats.exponweib.cdf(x, a=1, c=i)

ax[1].plot(x, y_cdf, "-", label=f"weibull dist cdf c: {i}, a: 1")

ax[1].set_xticks(x_tick_s)

ax[1].legend()

plt.show()

interestingly if we put c or k = 1

then \(f(x;\lambda) = \lambda e^{-\lambda x}\)

it becomes exponentiated exponential distribution and it is true also, as with a constant event rate Weibull distribution changes to exponential distribution.

Points to note#

For events that occur at a constant rate, the number of events per unit of time or space can be modeled as a Poisson distribution.

In this scenario, you can also model the time or distance between one event and the next as an exponential distribution.

A changing event rate over time (e.g., an increasing probability of device failure) can be modeled with the Weibull distribution.